According to a new analysis of homeowners insurance rates, some Midwest states saw the biggest jumps in premiums last year—and American Family �˽�����ýӳ�� topped a list of 10 insurers ranked by average rate change.

The analysis this week is based on homeowners rate filings approved through Dec. 27, 2024—so not quite the whole year last year.

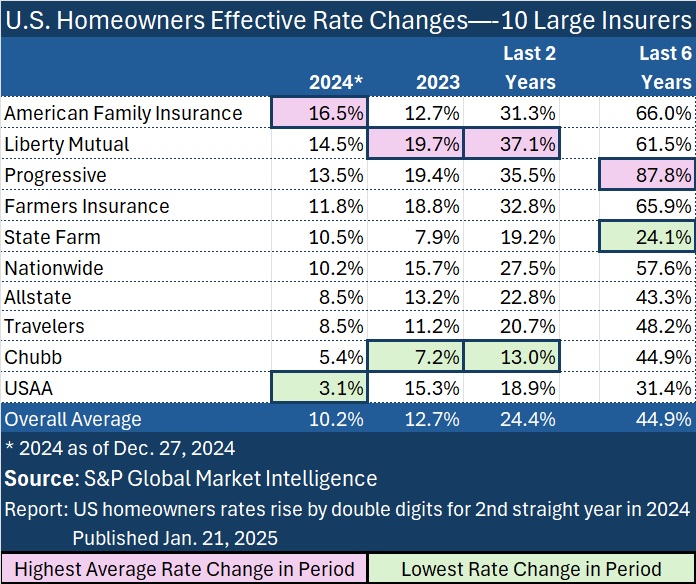

According to S&P GMI, the calculated weighted national average effective rate increase for homeowners insurance was 10.4% last year through late December. In 2023, the comparable figure was 12.7%, putting the two-year average increase at roughly 24 percent.

The state for which S&P GMI calculated the biggest effective rate increases for 2024 was Nebraska with 22.7%. In total, 33 states had double-digit calculated effective rate increases last year, with rates in Montana, Iowa, Minnesota, Utah and Washington also rising more than 20% by S&P GMI’s calculations.

Minnesota and Iowa were also among the states with the highest direct loss ratios in 2023 (including defense costs), although Hawaii, Kentucky and Arkansas were worse.

On the other end of the spectrum, Florida had the lowest—at 1.0%—but the text of the report notes that Florida’s calculation does not include any changes by Citizens Property �˽�����ýӳ�� Corp., the state-backed insurer of last resort.

For American Family, which raised rates in 42 states last year, the carrier’s three largest weighted-average rate increases occurred in Missouri (30.1%), Illinois (27.5%) and Nebraska (27.1%), the S&P GMI report says.

While the Wisconsin-based mutual insurer pushed rates up more than 31%, on average, countrywide in the last two years, the largest homeowner insurer, State Farm, ranks in the middle of the pack in terms of rate hikes with a two-year average increase of less than 20% across all states.

In fact, while the 10 insurers analyzed by S&P GMI increased homeowners rates by about 45% over the six-year period from 2019-2024, State Farm scored the lowest six-year jump at 24%.

Another mutual, Liberty Mutual, implemented the second-highest weighted-average rate change calculated by S&P GMI across the country, at 14.5% in 2024, and the largest two-year jump (of about 37%).

The text of the S&P GMI report provides more information about the states in which Liberty Mutual, Progressive and Farmers boosted rates the most, and includes a state-by-state chart listing overall average rate changes for the 10 insurers combined for each of the years 2019-2024.

Profitability Improves

Separately, rating agency AM Best published an analysis of loss ratio changes by line through the first nine months of 2024, finding that homeowners was the most improved line, driven by an aggressive push for rates.

Overall, the homeowners loss ratio experienced a 13.8-point improvement during the first nine months of 2024, compared to the same period in 2023, according to the report titled “ which summarizes data derived from U.S. P/C carriers’ third-quarter statutory statements (received and aggregated as of Jan. 6, 2025).

Across all lines, the loss ratio dropped 5.4 points, and AM Best said the significantly improved direct underwriting results were driven by increased earned premiums, which have outpaced the rise in incurred loss and loss adjustment expenses, and other underwriting expenses.

“The personal lines segment saw the most notable improvement, benefiting from an aggressive push for more adequate rates, pricing segmentation in personal auto, the impact of underwriting initiatives and improved catastrophe risk management practices,” AM Best said, noting that the improvement for the homeowners line came in spite of Hurricane Helene, which impacted third-quarter results.

David Blades, associate director, Industry Research and Analytics, AM Best, noted that although the nine-month results provide “optimism for full-year direct and net results, Hurricane Milton, which occurred in the fourth quarter, is expected to have a greater impact on homeowners and commercial property results than Helene.”

Commercial property was the second-most improved line in terms of underwriting profit, with the loss ratio for that line dropping 10.7 points.

Close behind, the personal auto segment’s direct loss ratio through third-quarter 2024 improved by nearly 10 percentage points and experienced an industry-leading 14% increase in direct premiums written.

Direct premiums written across the property/casualty industry were up by 9.1% compared with the same period in 2023, slightly below the 10.2% increase through third-quarter 2023.

Earlier this week, Travelers, the first publicly traded insurer to announce full-year earnings, reported increased underwriting profits for the company overall, but the biggest combined ratio improvement was a 10.4 point year-over-year drop for its personal insurance segment (10.7 points for homeowners and 10.0 points for personal auto).

Travelers full-year combined ratio for the homeowners line landed at 93.9, in spite of more than 24 points of catastrophe losses. The carrier reported renewal premium changes averaging 14.1% in the fourth quarter of 2024.

Topics Trends Pricing Trends Homeowners

Was this article valuable?

Here are more articles you may enjoy.

Worker Struck and Killed by Airplane Tug at Charlotte Airport

Worker Struck and Killed by Airplane Tug at Charlotte Airport  American Airlines DC Aircraft Collision Leaves No Survivors

American Airlines DC Aircraft Collision Leaves No Survivors  Lawsuit Accuses Amazon of Secretly Tracking Consumers Through Cellphones

Lawsuit Accuses Amazon of Secretly Tracking Consumers Through Cellphones  Target Becomes Latest Company to Backtrack on DEI Initiatives

Target Becomes Latest Company to Backtrack on DEI Initiatives